5 months ago

46

5 months ago

46

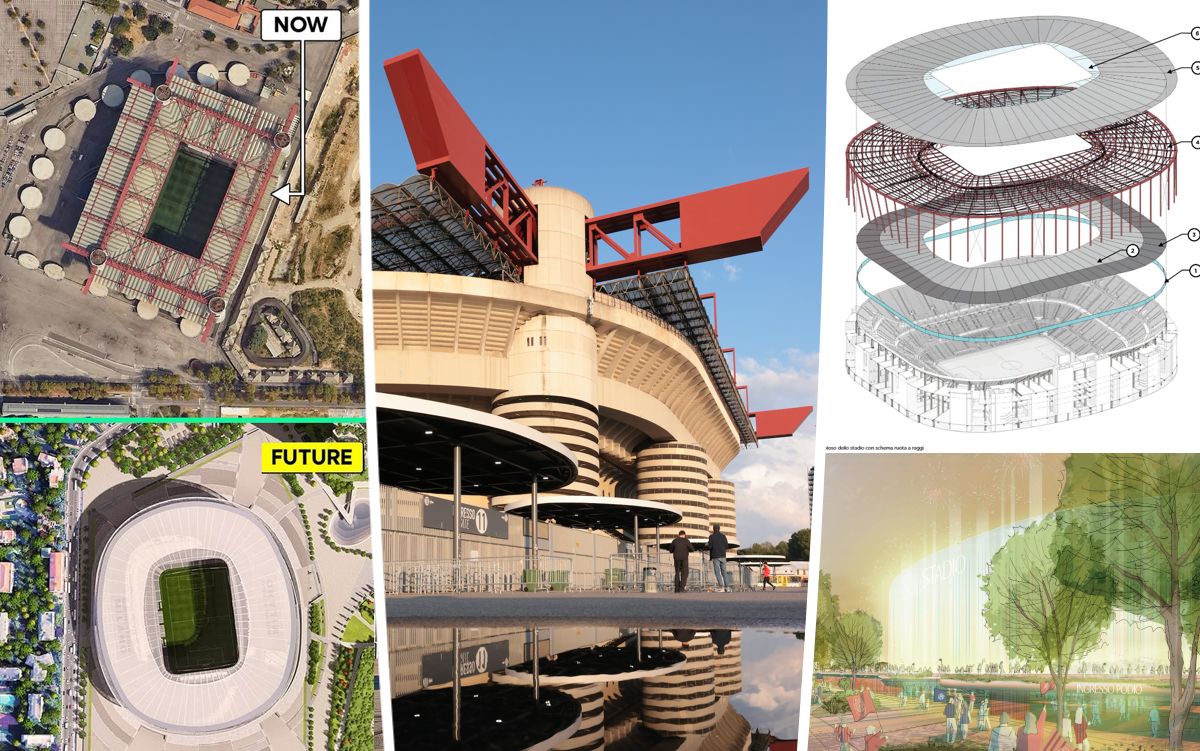

The corporate structure that will allow Inter and AC Milan to acquire San Siro and begin construction of the new stadium is now ready, a report claims.

According to Milano Finanza (via Calcio e Finanza) the two clubs have created two dedicated companies: Blueco, wholly owned by Inter, and Red Stadco, wholly owned by Milan. These are two special purpose vehicles created and managed separately.

How it works

They own in equal parts (50% each) NSM Holding, the company that by October will take over the San Siro from the Council and the building rights on the San Siro area, where the new stadium and the related real estate project will be built.

Blueco and Red Stadco were incorporated shortly before the decisive vote from the City Council last week. For Milan, President Paolo Scaroni appeared before a notary. For Inter, it will be Massimiliano Catanese, Nerazzurri chief of staff and Oaktree’s contact in the club’s organisational chart.

Filippo Guidotti Mori – AC Milan’s administrative and financial director from February 2025 – has been appointed to lead Red Stadco, while Inter has chosen Andrea Accinelli, the club’s CFO since 2021. The presence of the financial heads of both companies underlines the strategic importance of the stadium project, both for the clubs and for the Oaktree and RedBird funds.

The symbolic value of this operation is also evident in the birth, on October 3, of NSM Holding, the company that will manage the new Milan stadium. The headquarters have been set to Piazzale Angelo Moratti, right where the Meazza is located.

The six-member board of directors includes representatives of the teams and their respective funds: Inter’s board includes Catanese, Carlo Ligori (vice president of Global Opportunities at Oaktree) and Katherine Ralph, a leading manager at the American fund.

Milan’s board includes Guidotti Mori, Stefano Cocirio (the Rossoneri’s CFO), and Francesco Bramante, who is a representative of RedBird. Furthermore, NSM Holding’s bylaws include a pre-emption clause allowing one of the two clubs to take over the project should the other decide to withdraw.

The structure leaves open the possibility of new minority shareholders, which could be either the Oaktree and RedBird funds themselves or external investors. However, the shares can be used as collateral for financing, thus leveraging the value of the special purpose vehicle and holding company shares as collateral to secure credit.

This corporate structure offers clubs greater financial flexibility, allowing for the entry of supportive investors and reducing the debt required for the construction of the new stadium, a role that the Oaktree and RedBird funds themselves could also play.

Finally, the defined structure allows both funds to more easily plan a future exit from the clubs’ capital, even with different timeframes.

English (US) ·

English (US) ·